{kind=link}

ZCCM-IH MUST BE ALLOWED TO RUN MOPANI-PROF CLIVE CHIRWA

…Shareholders must reject the offer from IRH…

●Africa imports into the continent about 94% of copper wire and cables for building construction.

This is US$51.39 Billion per year market

I was astonished to see Mopani in that faded light.

It was a sad story that has to be regenerated in national interest.

I have a plan of how to revive the mining company under 100% ownership by ZCCM-IH PIc.

Finance and Labour are not part of the problems.

Here are simple draft calculations I have carried out showing Mopani

can remain Zambian for good and prosper bringing into the Zambian Revenue Authority coffers the revenue in Billions of Dollars every year since we have already paid U$$1.5 Billion in 2021 for it.

This is a Zambian company period.

Here are the

calculations to support my decision:

PROFESSOR CLIVE CHIRWA, PhD, DSc

FORUM: ZCCM-IH EXTRAORDINARY GENERAL MEETING – 23 February 2023 at 10:00hrs

UBJECT PROPOSAL: US$1.1 Billion by INTERNATIONAL RESOURCES HOLDING RSC LIMITED for 51% shares of MOPANI

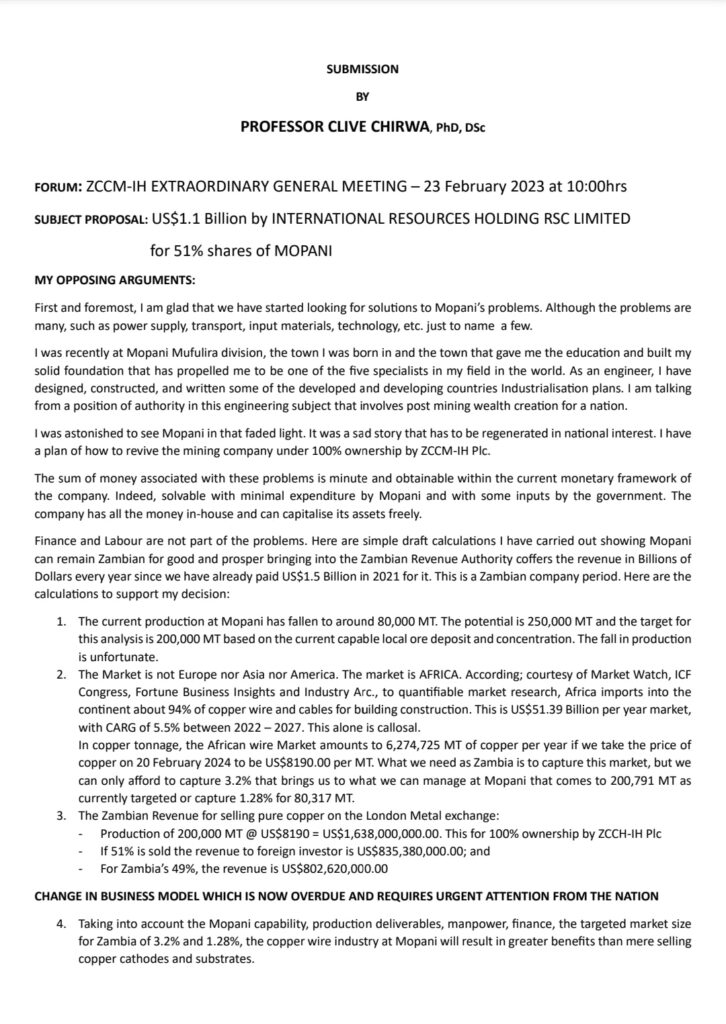

MY OPPOSING ARGUMENTS:

First and foremost, I am glad that we have started looking for solutions to Mopani’s problems.

Although the problems are

too many, such as power supply, transport, input materials, technology, etc. just to name a few.

I was recently at Mopani Mufulira division, the town I was born in and the town that gave me the education and built my

solid foundation that has propelled me to be one of the five specialists in my field in the world.

As an engineer, I have designed, constructed, and written some of the developed and developing countries Industrialisation plans.

I am talking from a position of authority in this engineering subject that involves post mining wealth creation for a nation.

I was astonished to see Mopani in that faded light. It was a sad story that has to be regenerated in national interest. I have a plan of how to revive the mining company under 100% ownership by ZCCM-IH PIc.

The sum of money associated with these problems is minute and obtainable within the current monetary framework of

the company.

Indeed, solvable with minimal expenditure by Mopani and with some inputs by the government.

The company has all the money in-house and can capitalise its assets freely.

Finance and Labour are not part of the problems. Here are simple draft calculations I have carried out showing Mopani

can remain Zambian for good and prosper bringing into the Zambian Revenue Authority coffers the revenue in Billions of

Dollars every year since we have already paid U$$1.5 Billion in 2021 for it.

This is a Zambian company period.

Here are the

calculations to support my decision:

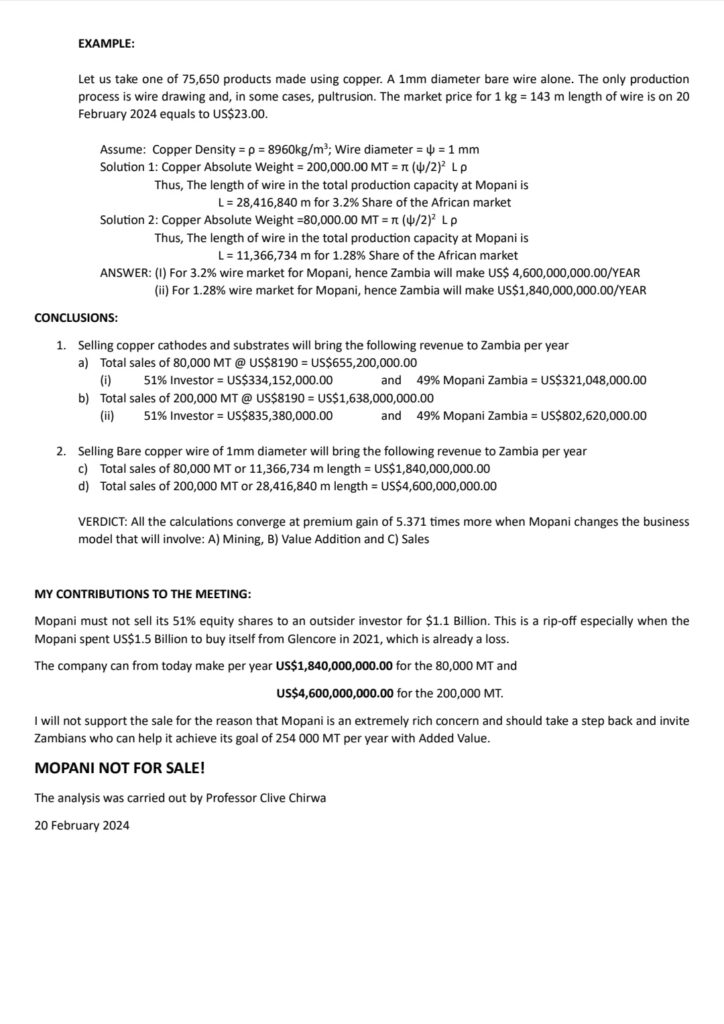

1. The current production at Mopani has fallen to around 80,000 MT. The potential is 250,000 MT and the target for

this analysis is 200,000 MT based on the current capable local ore deposit and concentration.

The fall in production is unfortunate.

2. The Market is not Europe nor Asia nor America.

The market is AFRICA. According; courtesy of Market Watch, ICF

Congress, Fortune Business Insights and Industry Arc., to quantifiable market research, Africa imports into the continent about 94% of copper wire and cables for building construction.

This is US$51.39 Billion per year market, with CARG of 5.5% between 2022 – 2027. This alone is callosal.

In copper tonnage, the African wire Market amounts to 5,274,725 MT of copper per year if we take the price of

copper on 20 February 2024 to be US$8190.00 per MT. What we need as Zambia is to capture this market, but we

can only afford to capture 3.2% that brings us to what we can manage at Mopani that comes to 200,791 MT as

3.

US

currently targeted or capture 1.28% for 80,317 MT.

the Zambian Revenue for selling pure copper on the London Metal exchange:

3.

>roduction of 200,000 MT @ US$8190 = US$1,638,000,000.00.

This for 100% ownership by ZCCH-IH Plc

If 51% is sold the revenue to foreign investor is US$835,380 000.00; and

For Zambia’s 49%, the revenue is US$802,620,000.00

CHANGE IN BUSINESS MODEL WHICH IS NOW OVERDUE AND REQUIRES URGENT ATTENTION FROM THE NATION

4. Taking into account the Mopani capability, production deliverables, manpower, finance, the targeted market size for Zambia of 3.2% and 1.28%, the copper wire industry at Mopani will result in greater benefits than mere selling

copper cathodes and substrates.

Theories are very easy to postulate but reality is completely different. The man is just making assumptions just from his thoughts not from what is practical and on the ground. For instance, he talks about Africa importing copper cables. If it was that easy to make money for Mopani, why has ZCCM-IH struggled to do so from the time they got the mine? And it’s not only ZCCM-IH that has faced challenges with running Mopani mine, Glencore had over $2.5bn in liabilities by the time they sold it to ZCCM-IH and that is the main reason they were so eager to let go of the time. Further to that, Mopani was making over $80mn in losses on a monthly basis according to their financial report at the time. If truly mining is so lucrative, why don’t these people who claim they can run mines open a greenfield mine so that we see how they fair instead of making wild claims which are not practical?

Furthermore, he connects Africa’s importantation of copper cables to running of Mopani which really does not make sense. The issue is that most African countries do not have value addition for their raw materials they produce hence importation of the finished products like cables and owning and running the mine won’t change that but instead he should have proposed setting up of value addition industries to add value to the minerals which would in turn reduce the importation of finished products like cables which would also result in improved revenue generation of African countries.

Clive Chirwa looted the funds that were earmarked for Zambia Railways. Now he wants to come and loot again with his silly scheme.

Let him explain what happened to the euronond money

As a person with a deep understanding of mineral resource sector, having spent over 30 years in the industry at home and abroad; I can confidently say that what Clive Chirwa has proposed is absolute gibberish. His assumptions are wild and without base to stand on. It is devoid of technical details on resources and reserves, primary and secondary development requirements, mining equipment, hoisting capacities and constraints. Capital costs associated with the above. Its a waste of time to even talk about beneficiation. I won’t speak about metal marketing. I was not exposed to that. I know understand why the ZRL was such a bad idea under Chirwa. Prof please stick to what you know best crash science. An undergraduate/bachelor degree holder straight from university would have come up with a better write.

I will not talk about metal marketing as I was not exposed to that in my career. Suffice to mention that there are penalties to be paid if the product does not meet the specs in the offtake agreements. I now understand why the ZRL was such a bad idea under Chirwa. Prof please stick to what you know best crash science. A geology or mining undergraduate/bachelors degree holder straight from university would have come up with a better writeup/ proposal. Have mercy and patriotism to our country. Let’s not pretend to know it all. Let’s give our nation what we know best.. From crash scientist, to railways expert and now mines and minerals development . Tulekwata Insoni nechikuku mwebantu

Clive Chilwa doesn’t understand anything. He us one sided thinking. He doesn’t know the operations cost of running the mine. Why did Glencore sell the mine? Does he know the cost of running Mopani per month? Where aregoing to get the $300 million operations costs? Why did Mopan fail in the first place while FQM continued operating. Now I understand why he failed to run ZRL, instead chose to stay at Falls way apartments and spent all the money for operations paying his rentals. The Euro bond was finished and he ran away.

What Prof Chirwa has proposed is gibberish. He makes financial assumptions without addressing the physical assumptions and constraints. Some of these are resources and reserves, primary and secondary development, mining equipment, hoisting capacities, processing , metal marketing. Where is he picking the 1.28% copper grade from and the tonnes of ore? I now understand why the the ZRL was misconceived and why it failed. A little knowledge is dangerous. Take note all the knowing it all “experts”. This man was introduced to us by Fred mmembe’s post newspaper as crash science academician, next he was a railway expert and now he is a mining and minerals development expert!!!. My foot!. Prof please stick to what you know best. Crash science. It is my considerd view that a mining and/or geology undergraduate degree holder would have made a better write up. Not say that such write up would have even made it for a proof of concept study. I wonder whether the prof has taken the trouble of going through a feasibility study for a mining project. Its now probable that he went to lead ZRL transformation without a feasibility study.

[20/02, 23:55]Chavula: Prof Chirwa can do all the calculations he likes. The missing equation is Capital. There is no way government can provide capital not even Zambian individuals. Government can also not secure from international sources.

[21/02, 04:54] Chundu: Prof Chirwa’s analysis avoids stating clearly how capital for recapitalising is going to be sourced. Unfortunately, the mining business requires capital injection upfront before the desired production levels can be realized. If it was that simple to raise capital as insinuated by the good Prof, surely the government would have opted for the route he has floated.

[21/02, 07:40] Mwila: Bo Henry, it is not only capital he has not taken into account

He is measuring profitability of the profitability based on revenue only. The revenue figures he is quoting do not automatically imply that the mining operation is making a profit as the case is now. In 2022, the profit margin on FQM’s production was around 25%. He has also completely ignored to factor in cost of production, cost of capital, taxes etc in his presentation. He is further proposing that Mopani should venture into the establishment of copper wire manufacturing plants, which he has erroneously classified as value addition for the Company. Even in the past ZAMEFA was not part of the mining industry

Also If it was that easy DRC would be doing the same and we would be in competition for the African market he said is available. I also strongly doubt the size the African market which he states consumes over 6 million tonnes of copper annually. This figure sounds too huge, which is twice of the total production of Zambia and Congo.

Is this Clive Chirwa kabolala we know who ate Eurobond during Michael Chilufya Data?

He is a criminal and Criminals should not be allowed to lead.

Who gets rich from digging stuff out of the ground? Clive Chirwa PhD, should be helping with setting up secondary industry based on our mineral endowment. Is he up to the task? Unfortunately, it seems he talks more than he delivers. Where’s his mini bus assembly he promised at Kapiri Mposhi? He even showed us the prototype at an exhibition at Government Complex.

Whether chirwa is right or not. It’s time we grow up and start running out show period. Let’s run out mines simple.

Clive Chirwa if you are so sure about your proposal then put your money where your mouth is. Get together a consortium of financiers which should not be so difficult if what profits you are showing is true and then bid for the same 51% to take over the mine. You can’t be experimenting with GRZ money then when your project fails you don’t lose anything.

Prof. made an agreement without fully understanding the intricacies of the Mopani-Glencore deal. ZCCM-IH bought the mines on credit, hence, the $1.5 billion he referred to isn’t money that as paid off.

Secondly, glencore was to retain 80% of Copper revenue for a period of 17 years+.

Thirdly, Mopani was left to sort out the debt glencore left, while struggling to manage running costs.

His calculations are viable but they are based on misinformation.

Another issue I have is where was he since 2021 to come out and help solve the problem, seems like political rhetoric to me. Why publish this a few days before when he had three years to get involved?