{kind=link}

ABOUT THE MISSING K65M MILLION: DISECTING THE MOF EXPLANATION

By Sean E. Tembo – PeP President (MBA, BAcc, FCCA, FZICA, FCPA) Chartered Accountant & Registered Auditor

1. A few days ago, a local newspaper broke a story that K65,332,446 and US$57,950 which had previously been confiscated from Ms. Faith Musonda by the Anti-Corruption Commission (ACC) had gone missing and could not be traced. Apparently this local newspaper had intercepted a Draft Management Letter issued by the Office of Auditor General (OAG) to ACC in which the OAG was telling the ACC that the money which was alleged to have been transferred in the Consolidated Fund Account (Control 99) at the Bank of Zambia (BOZ) was in fact not reflecting in the said account. In the said Draft Management Letter which was leaked, the OAG further requested the ACC to provide an explanation why this was the case.

2. Once this story of the alleged missing K65 million broke, it elicited a very strong reaction from different quarters of Government and it’s agencies, including the Board Chairman for ACC, Mr. Musa Mwenya who held a press conference and offered his own explanations, the Ministry of Finance, which issued a statement giving its own explanations and the Republican President Mr. Hakainde Hichilema himself, who claimed that the said Draft Management Letter from OAG was a fake and essentially accused those who reported the story of being mischievous as the money was allegedly used to pay student meal allowances through the Higher Education Loans and Scholarships Board (HELSB).

3. Subsequent to this debacle, the Managing Editor of the local newspaper that broke the story about the missing K65 million was summoned by the Zambia Police Service Anti-Fraud Unit at Police Headquarters, together with the specific reporter who wrote the story. The Police Call Out in question was extensively widely circulated and to any reasonable observer, these two journalists were being summoned by Police in connection with the OAG’s Draft Management Letter which the President had claimed to be a fake. However, subsequent to their appearance and interrogation at Police Headquarters, the two journalists held a press conference at which they explained their encounter with the Police. Apparently, the Police did not ask them any questions regarding the missing K65 million story or the Draft Management Letter, but instead were asking them irrelevant questions about the shareholding structure of the newspaper! The two journalists however took the opportunity of their press conference to confidently reiterate that the Draft Management Letter from the Office of Auditor General regarding the alleged missing K65 million was genuine and they still stood by it.

4. From the day that the story about the missing K65 million broke, l was approached by several individuals and organizations to render my opinion on the matter, ostensibly because of my background as a Chartered Accountant and Registered Auditor who has been running an Audit Firm for more than 20 years in Zambia and the region. Also, the individuals and organizations that reached out to me on this matter knew, rightly so, that l would not flinch to tell the truth as l saw it, even if it made President Hakainde Hichilema uncomfortable or upset. However, for about a week now, l have resisted commenting on this matter until this very moment. The reason is simple; when a major scandal such as the alleged missing K65 million breaks, it is often an unfolding story meaning that as time passes, more affected parties will comment on the matter and more information will come to light. So as a matter of strategy, l often allow a scandal to mature before l comment on it, and by so doing, my comments are often premised on more available information from different affected parties. In this particular case, the President has commented, Ministry of Finance has commented, the Anti Corruption Commission has commented, the Zambia Police Service through their summons have commented and the Managing Editor of the local newspaper that broke the story has also commented through their press conference following their interrogation at Police Headquarters. I believe the time is now ripe for me to render my thoughts on this issue of the alleged missing K65 million.

5. Firstly, allow me to state that when conducting an audit, the issues raised in a Draft Management Letter are not final, and some of them are often explained away or audit evidence is provided to rebut the draft findings. Sometimes the client is just lazy to provide the information requested by us auditors on time, and since our work as auditors is time-bound, we often just proceed with putting our preliminary findings in a Draft Management Letter and throw it to the client. When the client sees the preliminary findings, they often scamper in all directions looking and providing us with information that we had requested from the beginning of the audit and that would rebut our preliminary findings. It’s a trick that works well to increase audit efficiency and ensure that audits are completed on time. That means the mere fact that the K65 million is alleged to have gone missing in the Draft Management Letter did not necessarily mean that indeed the money was missing as at that point before the Government could give their comments and explanations. Luckily for us however, we have since received explanations on the matter, not only from the ACC, as the Office of Auditor General had envisaged when they wrote the Draft Management Letter, but we now also have explanations from the Ministry of Finance as well as the Republican President himself. What l am going to do from here is to review these explanations from Government and make a determination of whether they make sense, in which case the K65 million is not missing, or they don’t make sense, in which case the K65 million is missing.

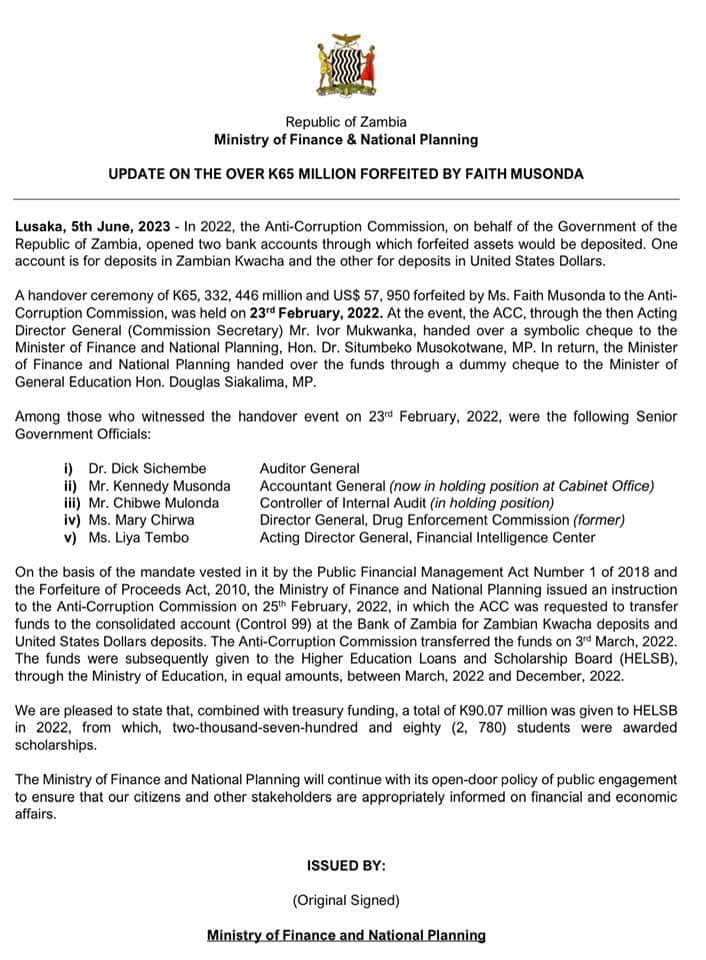

6. Our starting point is the official statement issued by the Ministry of Finance on 5th June 2023, which l have decided to attach to this article for purposes of convenience. In paragraph 1 of the statement, MoF says in 2022 ACC opened two bank accounts through which forfeited assets would be deposited. However the statement does not indicate on what date specifically the said bank accounts were opened, the name of the financial institution where these bank accounts were opened i.e. ABSA, STANBIC, STANCHART, ZANACO etcetera. Neither does this statement state the specific account numbers in question. When you are doing a forensic audit, one of the things to look out for are broad statements which are not specific and which are incapable of reconfirmation. If you give me an explanation, l need to be able to reconfirm your explanation for me to admit it as audit evidence. I would have expected the MoF statement to be in the lines of “On 17th May 2022, the ACC opened account number 123456 with XYZ bank for Kwacha deposits of forfeited funds and account 987654 with the same XYZ bank to deposit foreign currency forfeited funds”. Such a specific statement would constitute audit evidence because me as an Auditor l can go to XYZ bank and request for bank statements for those two alleged bank accounts so that l can see whether indeed the K65 million was deposited there or not, when it was deposited and when it was transfered out to the Consolidated Fund Account (Control 99) at BOZ. So far, the MoF explanations in paragraph one of their statement is empty and does not carry water. But let’s look at paragraph two and see what it holds for us.

7. Paragraph two of the MoF statement talks about the handover of a dummy ceremonial cheque by the ACC to MoF and subsequently to HELSB through Ministry of Education (MoE). However, this paragraph is irrelevant because a dummy cheque has nothing to do with the audit trail for the K65 million. That’s why it is called a DUMMY CHEQUE. From an audit point of view, we are only interested in the actual cash and if it is deposited in a bank account, the account number, the name of the bank, when it was deposited, when it was transfered out, whether it earned some interest while in that bank account, how much the interest was, what happened to the interest etcetera. Auditors are not interested in dummy cheques. However, l want you to take a moment and compare paragraph two of the MoF statement to paragraph one. What do you see? Take your time, don’t be in a hurry. Let me tell you. Paragraph two which talks about a useless dummy cheque is surprisingly very specific and detailed as it states the exact date when this dummy handover ceremony took place, where it took place, who participated in the handover and goes even further to list some of the high ranking Government officials who were present as witnesses including the then Auditor General; Dr. Dick Sichembe. If this was actual cash being handed over, then from an audit point of view it would constitute irrefutable evidence that indeed the K65 million was handed over from the ACC to MOF and subsequently to MoE. But there was no cash present at this ceremony, just a dummy cheque! So despite the long list of witnesses, this entire event is not proof that the K65 million moved from ACC to MoF to MoE. But as an Auditor, at this point l am very worried because of the eminent desire by MoF in their statement to over-emphasize the dummy cheque event which is useless, and fail to provide details relating to the bank accounts opened by ACC where the money was alleged to have been deposited. To me, it appears like a ploy to hoodwink the general public, most of whom are not financially literate. If the Ministry of Finance was sincere and honest, then the level of detail provided in paragraph two of their statement should have instead been provided in paragraph one. That is because paragraph one is important in establishing the audit trail for the alleged missing K65 million whereas paragraph two is irrelevant as it only talks about a dummy cheque. But let’s move on to paragraph 3 of the statement and see what it holds for us.

8. Unlike paragraph two which talks about a dummy cheque, paragraph three is talking about the actual movement of funds and is important to us in determining the audit trail for the alleged missing funds. However, you will note that the specificity which was very pronounced in paragraph two when talking about the dummy cheque has now disappeared. MoF is telling us that the ACC transferred the funds to the Consolidated Fund Account (Control 99) held at BOZ on 3rd March 2022 but does not tell us from which Bank the funds were coming from and also does not address the specific issue raised by the Office of Auditor General in their Draft Management Letter that the money was not reflecting in Control 99 at BOZ. Unlike you and me, the Office of Auditor General has access to the Consolidated Fund Account at BOZ, and are able to review each and every credit and debit on that account.

9. Indeed, the Ministry of Finance statement failed to explain why the money allegedly transfered by ACC, from God knows which Bank and account number, did not reflect in Control 99 at BOZ. If MoF had provided the OAG with the specific Bank and account numbers were ACC was keeping the K65 million, then the Auditors would have been in a position to check whether the money indeed left those bank accounts on 3rd March 2022, and it it did, why it was not reflecting in Control 99 at BOZ. Were the bank details used by ACC accurate? If so then why didn’t the monry land in the Consolidated Fund Account at BOZ? From an audit point of view, it does not matter how MoF claims the money was used. What matters is a clear audit trail from the actual cash seized from Ms. Faith Musonda to the deposit in the unnamed bank and unnamed account number, to the transfer to Control 99 at BOZ and from Control 99 to the HELSB bank accounts with a specific Bank which HELSB banks with. According to their Draft Management Letter, the Auditors could not see the money reflected in Control 99 at BOZ and neither could they see a transfer from Control 99 to the HELSB bank accounts. At this point, l want you to pay attention to a few telltale signs of possible deceit in the MoF statement. Firstly they say the money was transfered by ACC on 3rd March 2022 but they do not say whether the money reflected in Control 99, and if so on what date. In other words, MoF is answering a question which the Auditors did not ask, and are dodging to answer a question which the Auditors asked. In their Draft Management Letter, the Auditors did not say ACC did not transfer the money no, rather the Auditors said the money DID NOT REFLECT in Control 99 account held at BOZ. That was the specific finding of the Auditors, and MoF failed to address this finding in their statement. The second telltale sign of possible deceit by MoF is that their statement lacks ownership as it was not issued and signed by a specific person holding a specific position at Ministry of Finance. If there is false information in the statement, whom will law enforcement agencies hold responsible? If the statement was credible, why didn’t the Minister take ownership, or the Permanent Secretary or the Accountant General or the Secretary to the Treasury? Why being evasive by not including any name on the statement?

10. Having thoroughly and objectively examined this matter, it is my considered opinion that indeed the K65,332,446 and US$57,950 seized by the Anti Corruption Commission from Ms. Faith Musonda is missing, as determined by the Office of Auditor General in their Draft Management Letter addressed to ACC. It is also my considered opinion that the explanations provided by the President, by MoF, or by ACC do not address the issue raised by OAG in their Draft Management Letter. I also verily believe that this money is missing not because of some clerical error or mispost, but was diverted through a conspiracy by officials from ACC, MoF and State House. You might ask why l have included State House in this missing K65 million matter? Well, if State House was not involved, then President Hakainde Hichilema would not have passionately defended this missing money, to the extent of calling the Auditor General’s Draft Management Letter a fake. Additionally, the summoning of the local newspaper’s Managing Editor and reporter by Police Headquarters was ochestrated and designed to create a falls public perception that indeed the Draft Management Letter was a fake as claimed by President Hakainde Hichilema, when in fact not. The fact that Police Headquarters during their interrogation of the two Journalists decided not to ask any questions about the OAG Draft Management Letter means that the Police know that it is genuine, contrary to assertions by President Hakainde Hichilema. Also the fact that Police Headquarters was used to cast aspersions on the local newspaper, its Managing Editor and Reporter is evidence that someone high up in Government is involved in the missing K65 million and the plot to cover up the scandal. Someone high enough to use Police Headquarters to harass the local newspaper that broke the story. Someone in charge of the Police. Someone like the President. Indeed, President Hakainde Hichilema knows about the missing K65 million and is involved in the plot to cover up this scandal. For our part, the Zambian people can be rest assured that we shall pursue this matter to it’s logical conclusion. If it means petitioning the relevant Courts, we shall do exactly that. Daylight theft of public funds shall not be tolerated. It does not matter who the alleged thieves are or what positions they occupy in Government, they shall surely be held accountable.

///END

SET 12.06.2023